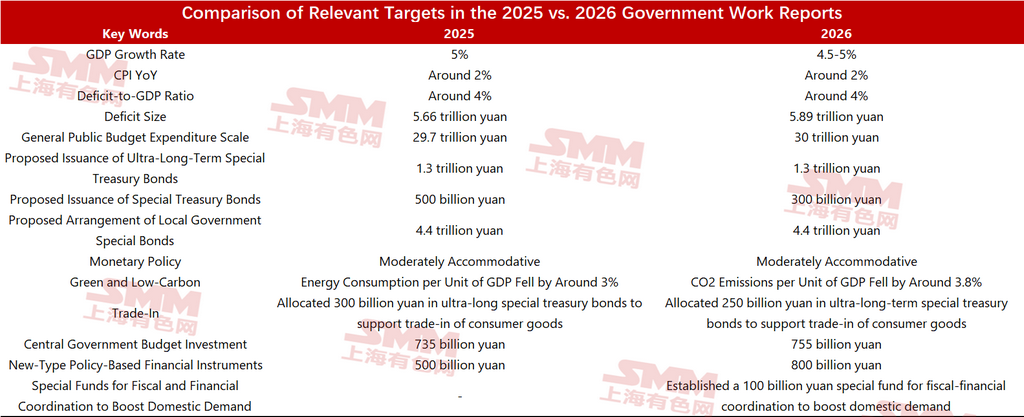

The Fourth Session of the 14th National People’s Congress opened at 9:00 a.m. on the morning of the 5th at the Great Hall of the People, where Premier Li Qiang of the State Council delivered the Government Work Report. Based on the relevant content of the Government Work Report, SMM compared the wording of certain core key words with that of 2025:

- Economic Growth Target

Both 2025 and 2026 set GDP growth at around 5%, with the 2026 target range at 4.5%–5%, basically flat versus 2025; Monetary policy: for two consecutive years, it has emphasized “implementing a moderately accommodative monetary policy” to keep liquidity ample.

Compared with 2025, some core indicators have changed—for example, the carbon-emissions target: in 2025, energy consumption per unit of GDP was to be reduced by around 3%; in 2026, this was adjusted to a reduction of around 3.8% in CO2 emissions per unit of GDP, taking into account multiple needs such as economic and social development, the green and low-carbon transition, and national energy security, and helping to achieve the goal of peaking carbon emissions before 2030 in an orderly manner.

- Deficit Size

5.89 trillion yuan, an increase of 230 billion yuan from the previous year.

- New-Type Policy Financial Instruments

issuance of 800 billion yuan in new-type policy financial instruments, an increase of 300 billion yuan from the previous year, which will effectively drive more private capital to participate in investment.

- Special Funds for Fiscal-Financial Coordination to Boost Domestic Demand

establish 100 billion yuan in special funds for fiscal-financial coordination to boost domestic demand, using a policy package of measures such as loan interest subsidies, financing guarantees, and risk compensation to support the expansion of domestic demand.

Overall, from a macro perspective, the policy package is gaining traction, focusing on expanding domestic demand and stabilizing growth. For the steel industry, the short-term macro environment is relatively supportive and is expected to lift market sentiment; over the medium and long-term, macro-level support is strengthening demand expectations, but attention is still needed on the pace of fund deployment.

![[SMM Steel] Morocco extends safeguard on HRC imports, posing new hurdle for Vietnam exports](https://imgqn.smm.cn/usercenter/aPBtI20251217171717.jpg)

![[SMM Steel] Nucor posts record shipments in Q1 on strong demand and project ramp-up](https://imgqn.smm.cn/usercenter/crVox20251217171717.jpg)